Once again, tariffs are the reason behind major market movements and supply chain disruptions.

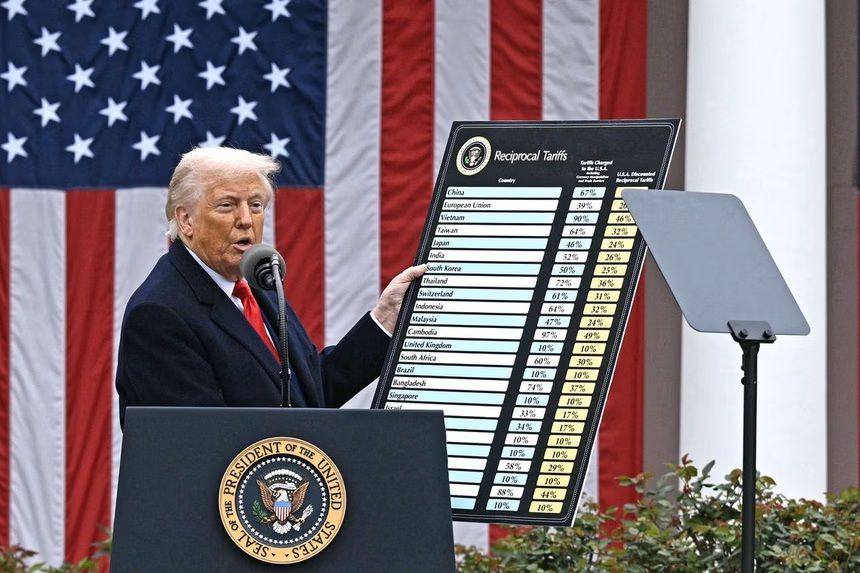

On April 2, President Trump announced a sweeping set of import duties, with effective rates ranging from 10% to 49%, targeting nearly every major US trading partner.

Since the decision was largely unexpected in scope and scale, it has already triggered a global selloff in equities, steep losses in consumer and tech stocks, and growing fears of long-term economic dislocation.

But which markets and stocks should investors worry about the most?

A brand new policy shock

The executive order introduces a baseline 10% tariff on all imports, with much higher country-specific rates.

Goods from Vietnam will now face a 46% levy.

Cambodia is subject to 49%, Indonesia to 32%, and Bangladesh to 37%.

China, already under previous tariffs, is now facing an additional 34% tax, bringing its total tariff burden to 54%.

Japanese imports are hit with a 24% rate, while the European Union faces 20%.

These measures have pushed the average US import tariff rate to around 22%, up from just 2.5% in 2024.

That’s the highest level since 1910, according to Fitch Ratings.

Trump framed the decision as reciprocal, claiming it reflects how other countries treat US exports.

But investors, analysts, and business leaders say the policy introduces new uncertainty and economic risk with no clear framework or timeline.

The financial markets reacted immediately.

US futures dropped sharply, with S&P 500 futures down more than 3%.

The Nasdaq has fallen nearly 13% since its December peak.

The yield on the 10-year Treasury dropped to 4.08%, its lowest level in six months, as investors fled to safety.

Global stocks followed.

Japan’s Nikkei fell more than 3%, while European markets declined around 2%.

In currency markets, the dollar index dropped 1.1% as traders priced in weaker growth expectations.

Footwear stocks got hammered

Footwear and apparel brands, many of which spent the past five years shifting production from China to Vietnam and Southeast Asia, were among the hardest hit.

For context, the US imported $136.6 billion in goods from Vietnam in 2024, up 19% from 2023.

The sudden 46% tariff on these imports has thrown cost structures and profit forecasts into disarray.

Nike saw its shares fall more than 8%, highlighting the company’s deep exposure to Vietnam, which produces 50% of its footwear and 30% of its apparel.

The brand has already lowered sales guidance for the current quarter, factoring in the expected cost increases from tariffs on China and Mexico.

These new Vietnam tariffs add further pressure.

Adidas shares dropped 11% in Frankfurt to near 12-month lows.

The German brand manufactures 39% of its footwear in Vietnam and relies heavily on factories in Indonesia (32%) and Cambodia (23%), all countries now hit by tariffs of over 30%.

Puma’s stock fell 8.5%, hitting its lowest level since November 2016.

The company has not issued formal guidance but, like Adidas, is structurally tied to Vietnamese and Indonesian factories for core product lines.

Swiss sneaker brand On Holding dropped 15% in US pre-market trading.

The company produces 90% of its shoes in Vietnam and another 10% in Indonesia, with nearly two-thirds of its revenue coming from the Americas, primarily the US.

According to regulatory filings, this makes it one of the single most exposed brands to the new tariff regime.

Deckers, the parent of Hoka and Ugg, has 68 production partners in Vietnam, its second largest manufacturing base after China.

Shares fell over 4%, reflecting concern over margin erosion.

Shenzhou International, one of Asia’s largest textile manufacturers and a major supplier to Nike, fell 18% in Hong Kong.

That’s its biggest drop in more than three years.

UBS and Jefferies estimate that brands would need to raise global retail prices by 5% to 12% just to preserve current profitability.

But with inflation-fatigued consumers, many may be forced to absorb the cost increases, eroding earnings.

Which tech stocks will struggle the most?

While the focus has largely been on consumer goods, tech companies are also under pressure.

The new tariffs hit Chinese imports with a combined 54% duty, and that includes nearly all devices assembled in the country.

Apple shares dropped 6.1%, the steepest one-day loss since September 2020.

Most of Apple’s hardware, including iPhones, iPads, and Macs, are assembled in China.

These goods now face the full brunt of the new policy.

The company has pledged a $500 billion US investment plan over four years, including a new manufacturing plant in Houston, but those facilities won’t mitigate near-term cost shocks.

Nvidia declined 4%. The firm designs chips in the US, produces them in Taiwan, and assembles AI systems in Mexico and China.

It remains vulnerable to component-level tariffs, especially if Taiwan and Mexico are next in line for tariff scrutiny.

Alphabet, Amazon, Meta, and Microsoft each lost between 2.5% and 5%.

The threat is indirect, that is, higher costs across consumer electronics and network hardware.

Nevertheless, it reflects broader fears of retaliatory digital taxes from the EU and Asia.

Retailers and supply chains take big hits

Beyond brands, large retailers with global sourcing operations were affected.

Wayfair dropped 12%, reflecting its deep exposure to Vietnamese-made furniture, which now faces a 46% tariff.

Walmart fell 6%, and Amazon lost 5%. H&M and Inditex dropped 4.5% and 3%, respectively.

These companies rely on textile and apparel factories in Vietnam, Bangladesh, and Cambodia.

Precisely the countries hit hardest.

Vietnam alone exported $44 billion in textiles in 2024, with the US as its top buyer.

Tariffs now impact nearly 10% of the country’s GDP, according to CEIC and OECD estimates.

Cambodia and Bangladesh face similar risks.

Attempts to shift manufacturing elsewhere are constrained by logistics, workforce specialization, and sunk costs.

Asian economies will struggle the most

Vietnam is the most exposed economy in Asia, with 12% of its GDP linked to direct and indirect US import exposure.

A 46% tariff puts an estimated 5.5% of Vietnamese GDP at risk.

Thailand faces a 3% hit, largely through auto exports.

Taiwan, while exempt from semiconductor tariffs, could see export volumes decline due to its dependence on the US market.

Currencies have begun to reflect these risks. The Vietnamese Dong fell to a record low of 25,803/USD.

The Thai Baht, Taiwan Dollar, and Indonesian Rupiah also came under pressure.

INR, PHP, and SGD are expected to outperform due to lighter exposure and steadier external balances.

Monetary policy expectations are shifting fast. Rate cuts are now expected in Korea, India, the Philippines, Indonesia, Singapore, and Australia.

These cuts range from 50 to 75 basis points as central banks aim to cushion the economic fallout.

The bottom line

The tariff regime is now shaping up to be a long-term paradigm change, especially if no exemptions or renegotiations are reached.

Trump has framed the move as a strategy to “pry open” foreign markets and force reindustrialization in the US.

But for companies, the challenge is immediate and severe.

Supply chain diversification, once a hedge against China risk, has now run out of options.

Vietnam and Indonesia, the main escape valves, are no longer viable under the current tariff structure.

Relocation isn’t a quick fix.

Performance footwear and advanced electronics manufacturing rely on highly specialized labor and infrastructure, which cannot be replicated overnight.

Tariffs have now become a persistent economic risk, not just a headline event.

The cost of global fragmentation is no longer theoretical, it is already hitting the balance sheets of companies around the world.

The post Tariffs hit global markets: who are the biggest losers? appeared first on Invezz